This blog is part of a series on Lean portfolio management. If you haven’t already, we recommend reading part one first, “What is Lean Portfolio Management,” which you can find here .

In the first installment of this series, we discussed why modern enterprises need Lean portfolio management and the specific elements that make Lean organizations better equipped to compete in a rapidly evolving, unpredictable world. In this post, we’ll discuss a fundamental component of Lean portfolio management: funding.

Funding practices—that is, the way budgets are allocated throughout the organization—dictate nearly every business outcome. Very little can be accomplished in an organization without the investment of time, money, and resources—so, it’s important to ensure that the way we make funding decisions aligns well with the business outcomes we’re trying to drive.

When implementing Lean-Agile practices at scale, organizations quickly realize that their push for agility conflicts with traditional budgeting and cost accounting practices. It’s not possible to truly achieve organizational agility without evolving these practices.

This is where Lean budgeting comes in. Adopting Lean-Agile budgeting practices helps to decrease funding overhead and friction while maintaining financial governance, helping to align budgeting practices with Lean-Agile goals.

Here are some of the main differences between traditional accounting practices and those used in Lean portfolio management.

The Problem(s) with Project-Based Funding

In traditional organizations, funding decisions are project-based, meaning budget is allocated on a per-project basis. Business units present their ideas to the PMO in an annual planning meeting. IT provides cost and time estimates and executives prioritize funding based on perceived value delivery in 12-18 months or longer. Then, teams get to work. Teams are incentivized to stay on track towards delivering the agreed upon plan and are measured according to how well they are able to stay on budget and on time.

As we discussed in the first post in this series, this structure results in deep inefficiencies across the organization:

- Project-based funding causes unnecessary overhead, bureaucracy, and delays

- Organizing temporary teams around projects (moving people to the work) results in low-performing, inefficient working groups

- Project-based funding requires detailed plans based on inaccurate projections, which takes time and people away from actually delivering value

- Planning on an annual basis creates a state of perpetual overload, which decreases productivity, morale, and throughput

- Progress is measured based on compliance to plan, instead of actual business outcomes or customer satisfaction

The root of each of these issues is the way work is funded and who controls the decision-making power around funding. In traditional organizations, this power resides with the PMO. In order to make informed decisions, the PMO requires teams to gather requirements and data and create plans for work that likely won’t be started for months. By the time the PMO receives the plan, it might already be out of date.

Funding a project might require pulling from multiple cost center budgets, creating a slow, complicated budgeting process that requires estimates, plans, and details far before they are able to be accurate. By the time a plan is approved, and the team begins work, it likely already has to be updated to account for new information, changing requirements, etc.

But accounting for new information might require additional paperwork—so teams are actually incentivized to not incorporate new learnings into the project.

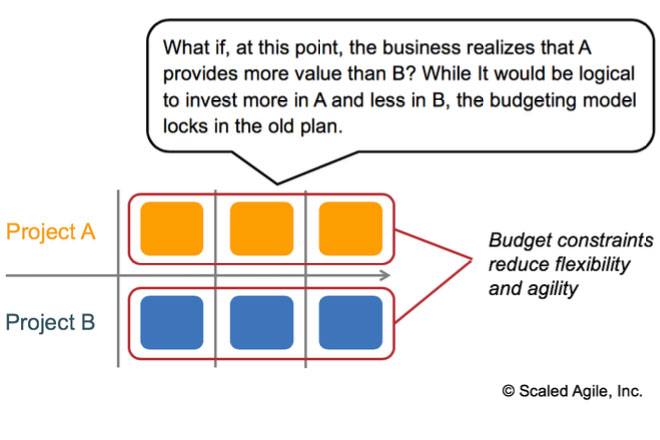

Once budgets have been approved and work is ready to begin, new challenges emerge. With project-based funding, budgets are fixed for the duration of the planned project.

The problem with this, of course, is that the people doing the work don’t have the ability to reinvest the budget based on the information they now have. In order to change the plan, they’d have to jump through hoops to re-budget and re-allocate team members to the more promising projects. Once again, the team is incentivized not to make this change—and the organization suffers as a result.

Estimates and Why They’re Unproductive

Certain types of work are highly predictable. A surgeon with 20 years of experience performing a simple procedure will likely be able to tell you exactly how long it will take, how many stitches will be needed, etc. before the work begins.

Other types of work are far less predictable, like software development or exploratory surgery. Sometimes, you don’t know what you don’t know until you get there. Work will take longer than expected because of new information and opportunities. This isn’t necessarily a bad thing—except that in a traditional environment, there is little room for these sorts of delays. Regardless of whether the work is creating value or not, once it exceeds the time allotted for it, it becomes a resource-draining problem—to which the next natural question is: Whose fault is this?

Using the example of exploratory surgery—if a surgeon was on the verge of finally fixing that issue in your rotator cuff, but he had told you the surgery would last two hours and was running out of time—would you want him to sew you up in order to stay on schedule, or finish the job? It seems like a silly question, and yet this is the situation we place our teams in when we fail to account for variability. Relying on estimates in a project-based model hinders cultural change, transparency, and solution development.

Lean Portfolio Management and Budgeting

Fund Value Streams, Not Projects

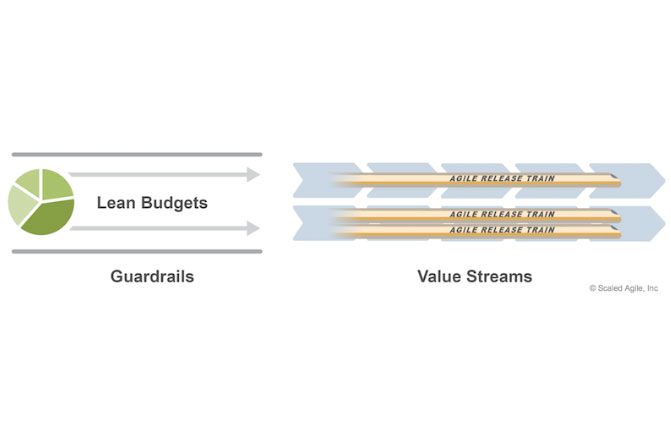

The term value stream describes the set of steps from the start of value creation until the delivery of the value to the customer. Organizations can form value streams around a specific product or solution, specific verticals, or in other ways, and might have several Agile Release Trains (ARTs) within each value stream.

Rather than trying to fund individual projects, the Lean approach allocates budgets to value streams, with guardrails to define spending policies, guidelines, and practices for that portfolio.

This provides ARTs with more autonomy for faster, better decision making. ARTs can self-organize to optimize resource efficiency, which also results in greater morale and job satisfaction. Small changes to the budget can be handled at the project level without having to escalate to management, which frees up management’s time for more strategic work.

Budgeting by value stream also makes it easier to measure organizational effectiveness, by simplifying the data collection required to assess performance. Budgets are typically fixed across a Program Increment (PI), but teams have the ability to prioritize or delay completion of work based on their actual capacity and are not penalized for not completing work according to inaccurate estimates. This means that teams are able to incorporate new information and learnings in real-time.

Participatory Budgeting

One of the many reasons that traditional budgeting methods inherently conflict with Lean thinking is that they create an unhealthy us vs. them environment in the organization. If all funding decisions are made by the PMO, then teams are inevitably pitted against each other, competing for resources instead of working to maximize their impact.

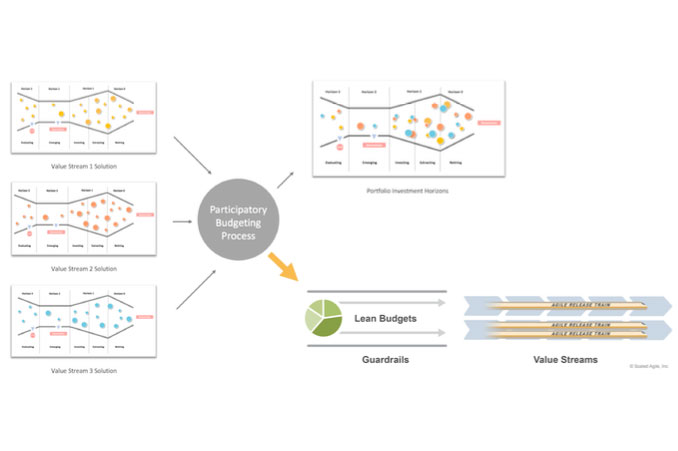

Participatory budgeting provides a healthier, more collaborative alternative to this approach. In participatory budgeting, business owners, stakeholders, and fiduciaries must work together to decide how to allocate investments. If several value streams are needed to complete an initiative, leaders have to decide how to pool their budgets. Although these conversations can be difficult, they result in a more informed, more inclusive system that ultimately makes the organization more effective.

The SAFe® investment horizon model can be used to ensure that decisions are tested and proven before they are presented. This model creates a forum where value stream leaders can share, learn, and help to ensure that the organization is making best use of its resources.

Remember, adopting Lean-Agile budgeting practices helps to decrease funding overhead and friction while maintaining financial governance, helping to align budgeting practices with Lean-Agile goals.

Continue reading the next installment in this series on Lean portfolio management:

Also, be sure to check out the whitepaper, “Lean Portfolio Management for the Enterprise.”